Deep Dives

Long-form research on finance and technology

The Intelligence Factory: AI Infrastructure

Disclaimer: This is not investment advice. This article examines ARK Invest's publicly available research report and stress-tests its claims. Nothing here should be taken as a recommendation to buy or sell any asset.

Big Ideas 2026, Part 2: The Intelligence Factory

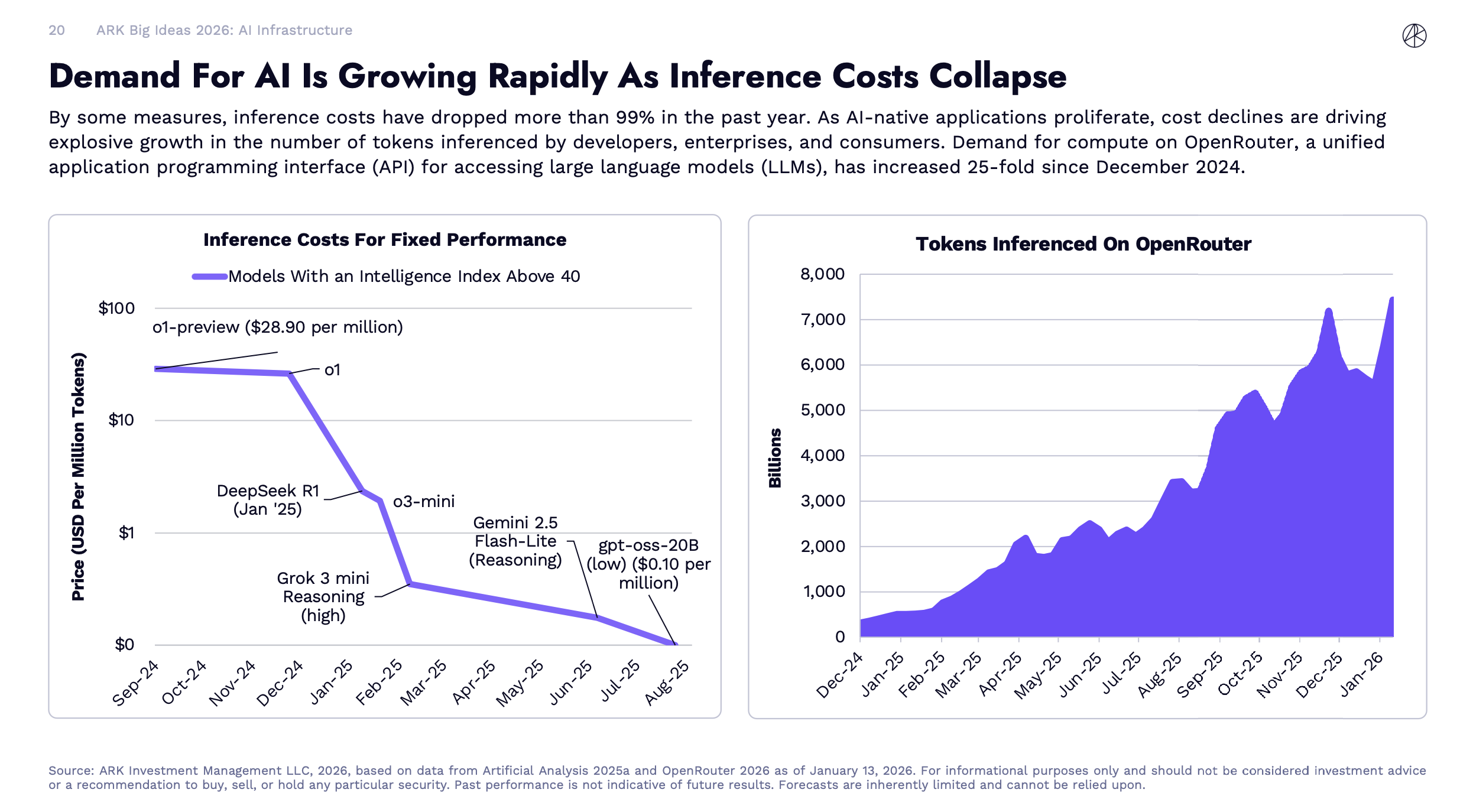

The cost of AI inference dropped more than 99% in a single year. That should settle the infrastructure debate. It makes everything more complicated instead.

The Big Picture

ARK's AI infrastructure report starts with Jevons' Paradox.

Inference costs have dropped more than 99% in the past year. As AI-native applications proliferate, cost declines are driving explosive growth in the number of tokens inferenced by developers, enterprises, and consumers.

Cheaper intelligence triggers Jevons' Paradox. The 19th-century economist William Stanley Jevons observed that more efficient steam engines did not reduce coal consumption. They made coal economical for new applications, and total consumption exploded. ARK is applying the same logic to AI, the cheaper each unit of intelligence gets, the more units get consumed. You do not save compute. You spend it on problems you never would have touched before.

Data Center

Data center capital investment is growing at 29% annually, ARK says, and will surpass $1.4 trillion cumulatively by 2030. Hyperscaler CapEx from the top five spenders (Amazon, Alphabet, Microsoft, Meta, and Oracle) is projected to exceed $500 billion in 2026 per ARK, with third-party estimates from IEEE ComSoc running even higher at $600 billion.

This is the structural bet behind the $1.4 trillion forecast. Not that AI gets more expensive. That AI gets so cheap it becomes infrastructure, like the way electricity or bandwidth became infrastructure, and total demand swamps any per-unit efficiency gains.

Whether that logic holds is the central question. ARK is not alone here. Goldman Sachs estimates data center power demand will rise 165% by 2030 compared to 2023 levels. The IEA reports AI-driven data centers already contribute roughly one-tenth of global electricity growth (and nearly one-fifth in advanced economies). The bet is widely held. That does not make it right, but this is not just ARK talking.

There's a Chinese idiom, 三人成虎, "three people claiming there's a tiger makes it feel real." The original warning is about false consensus, repeat something enough times and people believe it even if it's not true. But there's a flip side. When Goldman Sachs, the IEA, and ARK all point in the same direction, it's worth paying attention. Not because consensus equals truth, but because independent analysis converging on the same conclusion is structurally different from one firm talking its own book.

[subscribe]

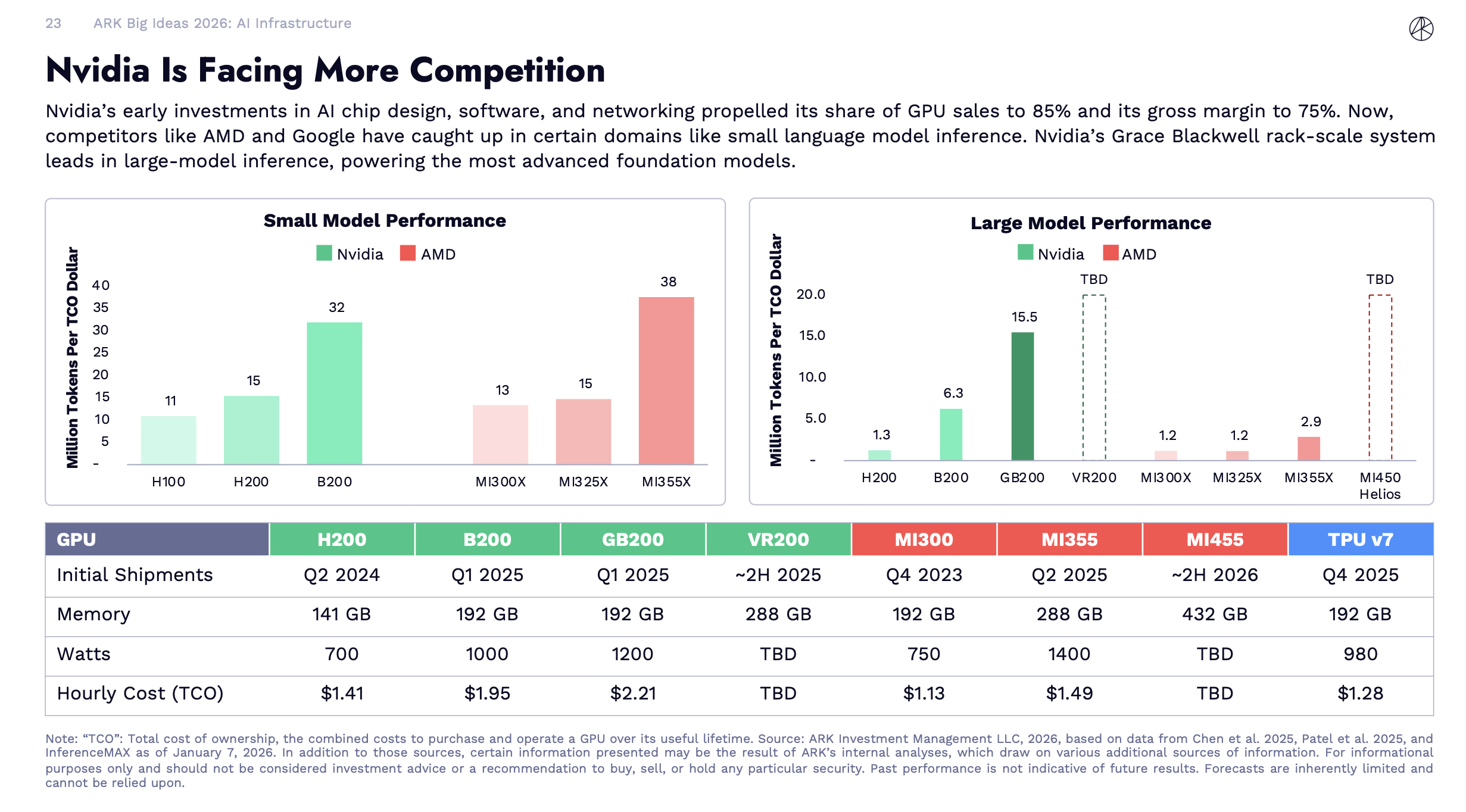

GPU Market (ok...My Favourite Part)

The GPU market is no longer a one-horse race, but the nuances matter.

This chart says, on large-model inference (the workload that powers frontier models like GPT-4 class systems, where hyperscalers concentrate their biggest budgets), Nvidia's GB200 still leads AMD's MI355X by 5-12x on tokens per TCO dollar. That is a commanding lead on the workload that defines who wins the biggest contracts.